Roth 401K Contribution Limits

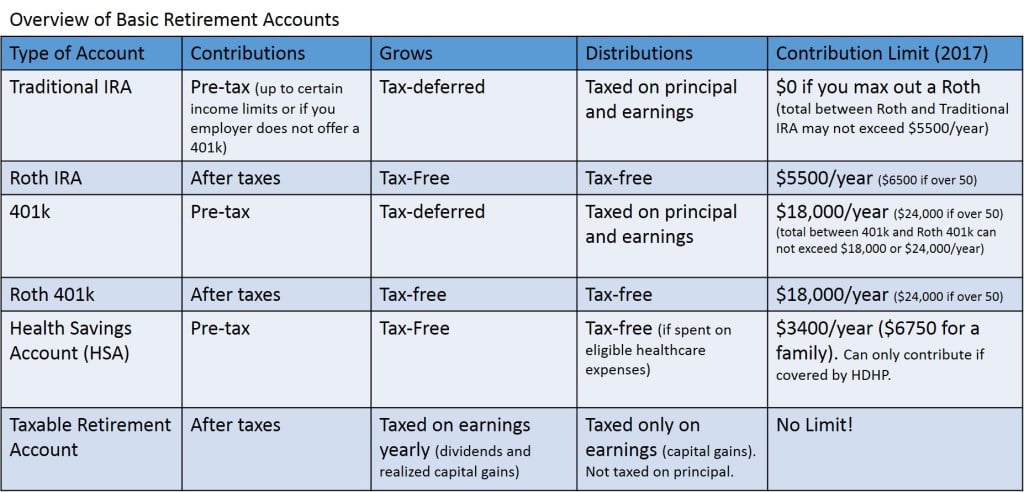

That brings the total contribution limit to $25, 000 for those who qualify. These new contribution limits also apply to 403(b), most 457 plans, and the federal government's Thrift Savings Plan. Tax Year Regular Contribution Limit Catch-up Contribution Limit for those 50 & older 2019 $19, 000 $6, 000 2018 $18, 500 $6, 000 2017 $18, 000 $6, 000 2016 $18, 000 $6, 000 2015 $18, 000 $6, 000 2014 $17, 500 $5, 500 2013 $17, 500 $5, 500 2012 $17, 000 $5, 500 2011 $16, 500 $5, 500 2010 $16, 500 $5, 500 2009 $16, 500 $5, 500 2008 $15, 500 $5, 000 2007 $15, 500 $5, 000 2006 $15, 000 $5, 000 IRA Contribution and Deduction Limits With a deductible IRA, it's important to understand both the contribution limits and the income limits to qualify for the deduction. While you can always contribute up to the $6, 000 contribution limit assuming you have sufficient earned income, you'll only be able to deduct your contribution on your federal taxes if you meet certain income limits. IRA Contribution Limits The maximum contribution in 2019 is $6, 000.

Roth 401k contribution limits for 2021

The "catch-up contribution" column applies only to people who are age 50 and older. The IRS allows older 401k participants to make additional contributions beyond the standard limits to encourage workers nearing retirement to increase their savings. The total contribution maximum limit tends to increase in $1, 000 increments. So far there haven't been a year where the contribution limits have decreased from the year before. Roth 401k Contribution Limits Roth 401k accounts have the same contribution limits as traditional 401k accounts. You can contribute up to $19, 500 to a Roth 401k plan, and up to $58, 000 in total if you are under 50 years of age. It is possible to have multiple 401k accounts. You can have both a Roth 401k and a traditional 401k and contribute to both plans at the same time as long as your contributions to both don't exceed the 401k limits. For 2021, you can allocate your employee salary deferral and employer's contribution however you choose between your Roth 401k and 401k retirement accounts as long as you don't exceed $19, 500 for the employee deferral and $38, 500 for the employer's portion.

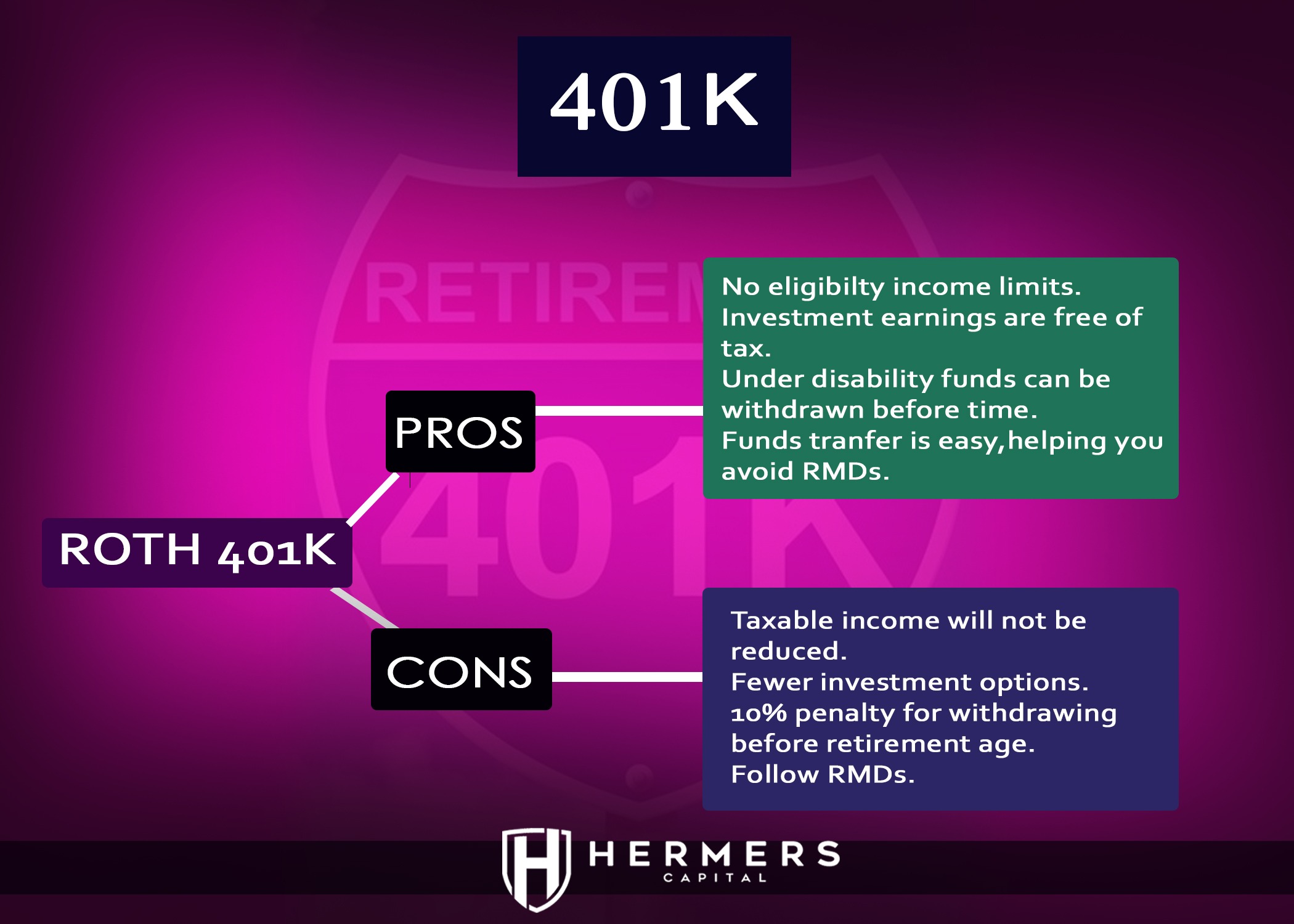

Key facts A Roth 401(k) is similar to a traditional 401(k) except that it requires you to pay taxes on contributions and does not require you to pay taxes on qualified withdrawals. The current annual contribution limit is $19, 500. You can contribute to a traditional and a Roth 401(k) and split the contributions in whatever way you wish, as long as the total amount is below the aggregate maximum contribution limit. A Roth 401(k) is an employer-sponsored retirement savings account that is funded with after-tax money. Because you've already paid taxes on the contributions, you do not need to pay any taxes on the distributions if certain conditions are met. What is a Roth 401(k)? A Roth 401(k) works in a similar fashion to a traditional employer-sponsored 401(k). The only difference is that with a Roth 401(k), contributions are made after your employer withholds taxes. Since you've already paid taxes on the contributions, you are not required to pay taxes on withdrawals provided they are qualified distributions.

The money in a 401(k) account can also be withdrawn without penalty if you become disabled, have a court order to pay out the funds due to a divorce, or your beneficiary withdraws the funds upon your death. Finally, you can take penalty-free withdrawals from your 401(k) for certain medical expenses, college tuition, or funeral expenses. You can also take the money for a down payment, repair of damage, or costs related to avoidance of foreclosure or eviction from your primary residence, but cannot withdraw it penalty-free to pay your mortgage payments. When a Withdrawal Penalty Applies While you can take money out of your 401(k) without penalty for several reasons, you'll typically still pay income taxes on it. If you just want to take the money out to do some shopping before you've reached 59 and 1/2 (or before 55 if the Rule of 55 applies to you), the IRS will hit you with a 10% penalty on top of taxes. That means that expenses such as a new car, a vacation, or upgraded furniture don't qualify as reasons to take out your 401(k) savings.

- Jet aircraft management

- Houston electricity company

- Have Questions about Associate Degree? Learn Directly from Our FAQs

- Roth 401k contribution limits highly compensated employees

- NYS Division of Licensing Services

- Roth 401k Contribution Limits 2021

- Roth 401k contribution limits 2020 over 50 years

- 401k and IRA Contribution Limits for 2019